New Construction vs Resale in Cape Coral: Which Makes More Sense in 2026?

Two houses, same street, same price — one built in 1994, one built last month. Which one's the smarter buy? In Cape Coral the sticker price is the number that tells you the least.

Picture two houses on the same Cape Coral street. Same four bedrooms, same three-car garage, same asking price to the dollar. One was built in 1994. The other came out of the ground last month. Which one's the smarter buy?

Most out-of-state buyers guess the resale — it's got the mature palms out front, the neighbors are already moved in, and older usually means cheaper, right? But in Cape Coral in 2026, that instinct can cost you real money every single month you own the place. Because the sticker price is the one number that tells you the least about what a home actually costs here.

So let's do the honest math — new construction versus resale — the way somebody who sells both would actually break it down. As of July 8, 2026, Cape Coral has 566 active new-construction listings on the market. Here's how they really stack up against the used ones.

The Sticker Price Is the Biggest Liar in the Room

Here's the trap. You pull up two listings, you compare the two big numbers at the top, and you think you've compared the homes. You haven't.

In Cape Coral, the median new-construction home sits around $450K. A comparable resale can list under that — sometimes well under — and that's the number that pulls out-of-state buyers toward the older home. Right now the median resale list price in the city is $400K, across 1,864 active resale listings, versus that $450K on new builds. And over the last 120 days, the resales that actually closed did so at a median of $365K — so yes, on paper, used looks cheaper.

But price is what you pay once. Carrying cost is what you pay for the next 360 months. And in Southwest Florida, the gap between a new home's carrying cost and an old one's isn't a rounding error — it's the whole ballgame. That gap has a name, and it's the thing no listing photo will ever show you.

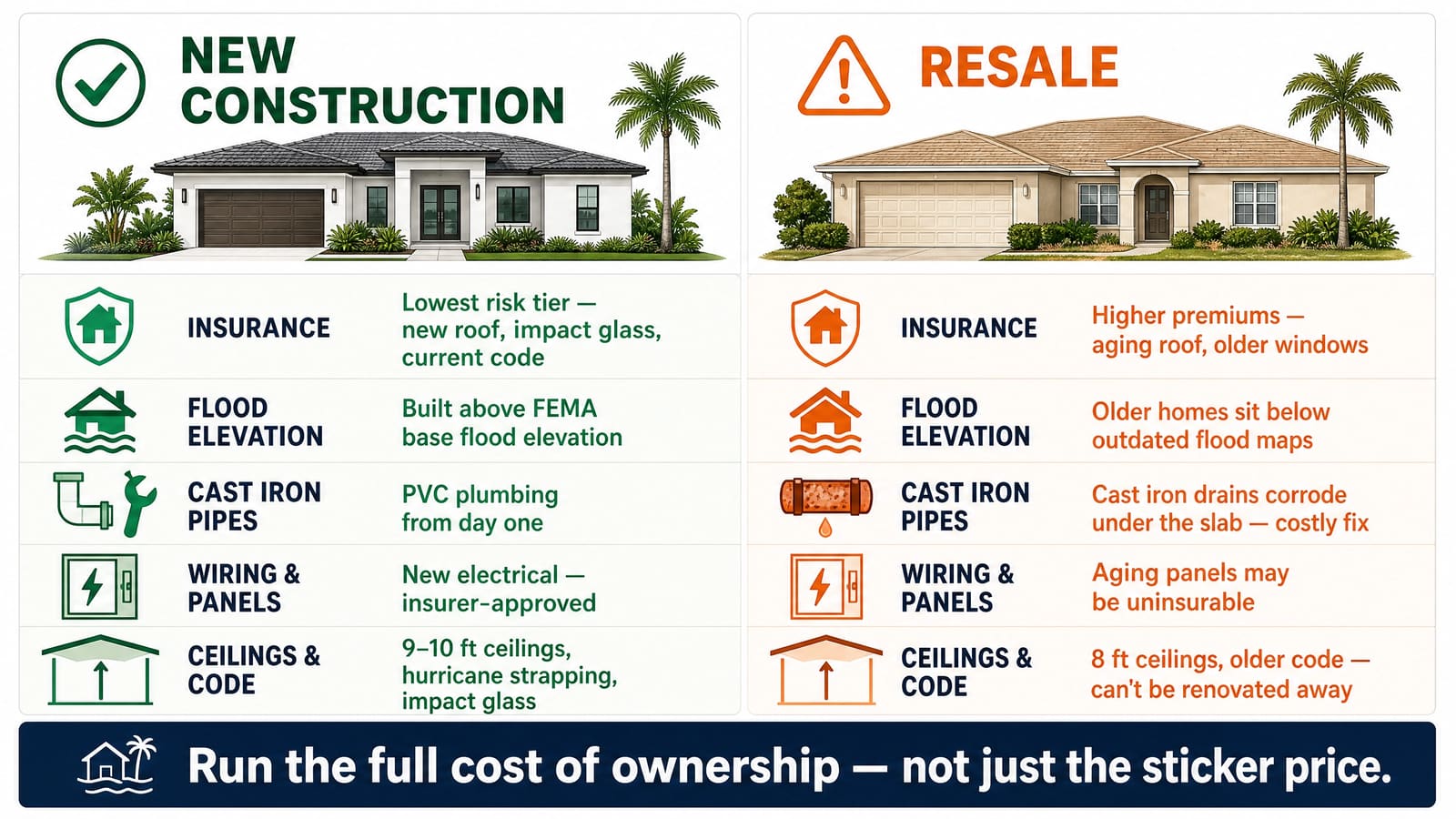

The Insurance Math Nobody Puts in the Listing

Let's talk about the number that actually decides this in Cape Coral: your insurance premium.

After the 2022 storm season and the property-insurance shakeout that followed, Florida carriers started pricing homes on one thing above almost everything else — the roof. A brand-new roof, new plumbing, new electrical, and new impact-rated windows and doors put a home in the cheapest risk bucket an insurer has. An older resale with a 15-year-old roof and original single-pane windows? Different bucket. Sometimes a much more expensive one, and in the worst cases, a home a carrier won't write at all until the roof gets replaced.

That's the swing. It's routine down here for a new-construction home to insure for a fraction of what a 1990s resale on the same block costs to insure — every year, forever. New homes also come built to the current Florida Building Code: impact glass or shutters, hurricane strapping, elevated slabs. Older Cape homes can be retrofitted, but you're paying for that out of pocket, and a wind-mitigation credit on an old house still won't match a new one built to today's code from the slab up.

Here's the skinny: when you add the insurance line and the "what am I going to have to replace in five years" line to the price, a new-construction home that looked more expensive on the sticker frequently comes out cheaper to own. That is the single most important sentence in this post.

Built Above the Flood Line — the Old Homes Weren't

Every new-construction home in Cape Coral has to be built to today's flood rules — the finished floor sits at or above FEMA's base flood elevation for that lot, and in many cases with a foot of "freeboard" stacked on top. Translation: new homes are built up, out of the water's reach by design.

A lot of the older Cape housing stock isn't. Homes that went up decades ago were built under older, lower flood maps — or before the maps meant much at all — and they sit low. Some of them noticeably below where a new home on the same street would have to start today. When the water comes, elevation is everything. That low finished floor is why an older home floods and the new one next door stays dry, and it's a big reason the older one costs more to insure — or, in the worst spots, why a carrier won't touch it.

And you can't cheaply fix it. You can replace a roof. You can't cheaply lift a 1970s slab home out of the flood plain. When you buy new here, the elevation comes baked in.

The Stuff Behind the Walls, Under the Slab, and Over Your Head

Now the things a walkthrough won't show you and a listing photo will never mention.

Cast iron pipe. A lot of Cape Coral homes from the '60s, '70s, and into the '80s were plumbed with cast iron drain lines — and cast iron doesn't live forever. It corrodes and collapses from the inside out. A failing cast iron system under a slab is one of the ugliest, most expensive surprises in an older Florida home, because fixing it can mean cutting into your floors. New construction is PVC from day one.

Old wiring and panels. Older homes can carry outdated electrical — aging or undersized panels, and the occasional problem-brand panel that insurers flat-out won't cover. That's another line item a resale can hand you, and another reason your premium quote comes back higher than you expected.

Low ceilings. Walk into a chunk of the older Cape stock and you'll feel it — eight-foot (or lower) ceilings that make the whole house feel smaller than its square footage says it is. New construction routinely runs nine- and ten-foot ceilings, tray details, and taller doors. It's the first thing buyers notice, and it's the one thing you genuinely cannot renovate into an old home without tearing the roof off.

None of this makes every resale a bad buy. It makes every resale a home you inspect with your eyes wide open — the roof, the wiring, the pipe under the slab, and how high off the ground the whole thing sits.

Here's the whole comparison on one card — the five costs that decide this market, side by side:

What Resale Actually Still Wins

Now let me not sell you mush — resale genuinely wins on some things, and I'm not going to pretend otherwise.

Location and lot. The older, established parts of Cape Coral — the ones closer to the water, closer to the bridges, on the wider Gulf-access canals — were built out first. A lot of the newest construction is on scattered lots in the outer sections, further from everything. If your heart is set on a seawall and a boat lift ten minutes from open water, a lot of that is resale, and there's no new-build substitute for it.

Mature everything. Real trees. Grass that's already in. A neighborhood that's fully finished instead of one where the lot next door might become a construction site next spring. Resale hands you a settled street on day one.

Speed of the market, honestly. Cape resales are moving — the actives are sitting at a median of just 66 days on market, and the ones that closed over the last 120 days went in a median of 48. If you're selling one to buy one, that liquidity is a genuine plus.

Price per square foot, sometimes. On an inland, dry-lot, cosmetically dated resale, you can occasionally buy more house per dollar than new construction — if you go in clear-eyed about the roof, the insurance, and the kitchen you're going to want to redo.

That's a real list. Resale isn't the wrong answer — it's the right answer for a specific buyer who values location and mature setting over carrying cost and wants to take on some risk to get there.

The 2026 Twist: The Builders Are Dealing

Here's what tilts the field this year. Cape Coral new construction is not a fire sale — 494 homes closed in the last 120 days at 98.9% of list, so sellers aren't giving these away. But at a median 102 days on market and 4.6 months of supply, builders have inventory sitting — notice that's half again as long as the 66 days the typical resale sits — and inventory that sits makes builders generous.

That generosity shows up as rate buydowns, closing-cost credits, and price adjustments on standing spec homes — incentives a private resale seller almost never matches, because a resale seller can't reach into a mortgage company and knock two points off your rate. A national builder's in-house lender can, and right now, they will. When you're comparing a new build to a resale, run the builder's incentive against the resale's list price before you decide the resale is cheaper. Half the time the incentive erases the gap.

Listen Up: How to Actually Decide

Here's the honest framework, and it's simpler than the internet makes it.

Buy new construction if your priority is knowing your costs. New roof, new systems, current-code build, the lowest insurance bucket in the market, a builder warranty, and — in 2026 — a builder who'll buy your rate down. You trade the established location for a home that's cheaper and less stressful to own, and you don't spend your first two years writing checks to contractors.

Buy resale if location and lot are the whole point — a specific Gulf-access canal, a mature neighborhood, a piece of the Cape you can't get in new construction — and you've priced the roof, the insurance, the wiring, the cast iron pipe, and the flood elevation honestly, and the number still works.

What you should not do is compare two sticker prices, pick the lower one, and call it a decision. In Cape Coral, that's how out-of-state buyers end up "saving" $50K on the purchase and handing it right back in premiums and a roof replacement. Run the whole cost of owning it, not just the cost of buying it.

💡 Key Takeaways

- In Cape Coral, the resale's lower sticker price ($400K median list vs $450K new-build median) is often erased by higher insurance, an aging roof, and updates — new construction frequently costs less to own.

- Insurance is the deciding factor here: a new roof, impact glass, and current-code construction put a home in the cheapest risk bucket carriers have.

- New homes are built above FEMA's base flood elevation; older Cape homes sit lower under outdated flood maps — the difference between flooding and staying dry, and a big driver of your premium.

- Watch the hidden stuff in older homes: cast iron drain pipe that corrodes, outdated wiring and panels, and low eight-foot ceilings you can't renovate away.

- Resale still wins on location, lot, and mature neighborhoods — especially the established Gulf-access canals the newest builds can't touch.

- 2026 builders are offering rate buydowns and closing credits a private resale seller can't match. Run the incentive before you call resale cheaper.

Frequently Asked Questions

Is new construction more expensive than resale in Cape Coral?

On the sticker, usually yes — the median new build in Cape Coral is around $450K as of July 2026, while the median resale lists at about $400K (and recent resales have closed at a median near $365K). But once you add insurance, roof age, and the cost of updating an older home, new construction frequently comes out cheaper to own on a monthly basis. Compare total cost of ownership, not just purchase price.

Why is insurance cheaper on new construction in Florida?

Florida insurers price heavily on roof age and construction standards. A new home has a brand-new roof, impact-rated windows and doors, and is built to the current Florida Building Code — which puts it in the lowest-risk, lowest-premium category. Older resale homes with aging roofs and original windows can cost significantly more to insure, and some carriers won't write them until the roof is replaced.

What should I inspect on an older Cape Coral home that a new build doesn't have?

Four things out-of-state buyers routinely miss: the roof's age (it drives your insurance), cast iron drain pipes (common in homes from the '60s–'80s, and they corrode and fail under the slab), the electrical panel and wiring (older or problem-brand panels can raise premiums or be uninsurable), and the home's flood elevation. New construction has to be built above FEMA's base flood elevation; older homes were built lower under outdated maps. Get all four checked before you compare an older home's price to a new build's.

Are there good resale deals in Cape Coral in 2026?

Yes — especially on inland, dry-lot homes that are cosmetically dated, and in established Gulf-access neighborhoods you can't buy new. Resales are also moving faster than new builds right now (a median 66 days on market versus 102 for new construction), so the good ones don't linger. Just factor in the roof, the insurance premium, and any updates before you compare it to a new build. A resale that looks cheaper on paper isn't always cheaper to own.

Do builders in Cape Coral offer incentives that resale sellers don't?

They do. With a median 102 days on market and 4.6 months of supply, Cape Coral builders are offering rate buydowns, closing-cost credits, and price adjustments on standing inventory. A builder's in-house lender can lower your interest rate in ways a private resale seller simply cannot, so always price the incentive into your comparison.

Should a first-time or out-of-state buyer choose new or resale in Cape Coral?

For most out-of-state buyers who want predictable costs and less risk, new construction is the safer starting point — new systems, lower insurance, a warranty, and 2026 incentives. Choose resale when a specific location or lot (like an established Gulf-access canal) matters more to you than carrying cost, and you've priced the older home's true costs honestly.

See What's Actually Available

The market changes every week as homes list and close. See it live, filtered by what actually matters to you:

- Every active new build in Cape Coral

- New construction under $400K

- Compare every builder in one place

- Canal & Gulf-access new construction

Not sure whether a new build or a resale fits your budget, your timeline, and your tolerance for a roof project? That's the whole reason we're here.

If you need help buying in Cape Coral, call us at (239) 422-7459 and we'll run the real cost of owning both — sticker, insurance, and all — so you're comparing homes, not just price tags.